No Bullshit Guide into DeFi Lending & Borrowing: Collateral and liquidation

Collateral and liquidation are significant components of DeFi lending and borrowing. Understanding the two ideas is crucial since collateral is a requirement before borrowing and liquidation is how lenders may make money.

1. COLLATERAL

As we have mentioned in the previous article, collateral in DeFi borrowing landscape is usually 100% crypto asset. It has following feature:

- Loan to value (LTV) ranging from 0 - 85%, but never above 100%

- Assets with 0% LTV ratio CANNOT be used as collateral.

- Liquid assets will have higher LTV.

- Less liquid assets will have lower LTV.

- Usually LTV ratio is decided through the governance of the platform—depending whether its Compound, Maker, etc, each platform can have a different LTV ratio for the same asset.

- The reason why DeFi loans are always overcollateralized (usually LTV not exceed 90%, or collateralization ratio of at least 115%) are the asymmetric information and the collateral.

- Asymmetric information exists regarding the collateral & the borrower profile. Only the borrower knows exactly about his own profile and the quality of the assets provided as collateral, although the platform also makes decision related to whether or not they can accept an asset as collateral

- Collateral is a traded asset and some buffer needs to be made in relation to its value unlike RWA in which value do not fluctuate as much (for example properties)

- The implication is that DeFi loans are less capital effective compared to real life loan

2. LIQUIDATION & ROLE OF LIQUIDATORS

- User maintain user account in which liquidity is calculated as =

- When the amount borrowed exceed the total collateral supplied * collateralization factor, the account is in negative territory, and the collateral supplied will be eligible for liquidation.

WHAT IS LIQUIDATOR?

- Unlike in traditional markets, every transaction happening on Web3, and on any blockchains are not free. For example, Compound, dYdX, and Maker are all operating in the Ethereum network in which the gas fees are quite considerable.

- In short, Selling collateral and paying off loans will incur gas fees. This makes borrowers reluctant to pay since they will lose more money.

- Moreover, DeFi is pseudonymous with no KYC policy and no IDs being required upon undertaking a loan, etc. Borrowers will think "Why should I settle this account? No one knows who I am anyway! They cannot come after me, and besides, I’m already super upset with my collateral being underwater!"

- To solve these issues, DeFi has a party called liquidators who are secret whales lurking in the background and keeping the entire system solvent by liquidating underwater accounts in the red.

- Liquidators are incentivized by the portion of the collateral they liquidate. This metric is represented by the liquidator incentive multiple which is a number that is above the collateral seize size (protocol’s share)

- For example, an asset’s liquidator incentive is 1.08 and the collateral seize share is 1.06. This means, the liquidator will receive 2% incentive in form of the collateralized asset being liquidated, while the protocol keeps the remaining collateral

ILLUSTRATION

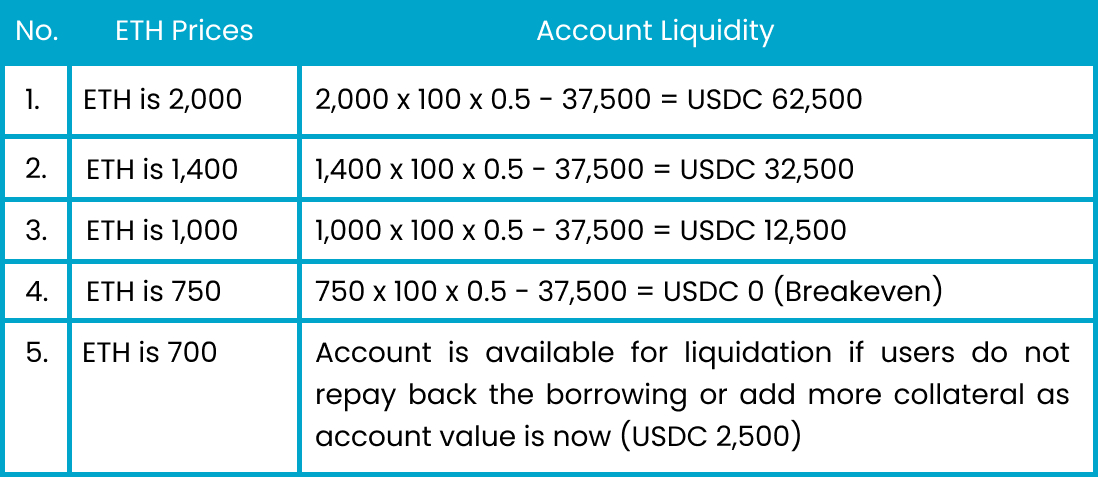

- Assume a borrower collateralized 100 ETH and the protocol’s LTV is 50%. Current ETH/USDC price is 1,500. Therefore, the max borrowed amount is 100×1,500×50%= USDC 75,000. Let's say our user borrow only half of the allowed amount i.e. USDC 75,000 /2 = USDC 37,500

- Account liquidity scenarios assuming different ETH prices

- ETH is 2,000 = 2,000 * 100 * 0.5 - 37,500 = USDC 62,500

- ETH is 1,400 = 1,400 * 100 * 0.5 - 37,500 = USDC 32,500

- ETH is 1,000 = USDC 12,500

- ETH is 750 = USDC 0 - breakeven

- ETH is 700 = account is available for liquidation if users do not repay back the borrowing or add more collateral as account value is now (USDC 2,500)

- Now let's say that the account is available for liquidation and the liquidation incentive is 1.07 while collateral seize share is 1.04

- Out of the 100 ETH collateralized, 3% will go to the liquidators (3 ETH)

- 4% will be added to the token’s reserves i.e. kept by protocol (4 ETH)

- The remaining 100 ETH - 7 ETH = 93 ETH will be returned back to the lenders who provide the funds for the loan

3. SUMMARY

- Collaterals are needed before someone can borrow from lending platforms.

- Collaterals in DeFi loans always have LTV ranging from 0-85%.

- DeFi loans are always overcollateralized since there is asymmetric information, price fluctuation, and it's less capital effectiveness.

- Collateral liquidation can be done when an account’s liquidity is below zero.

- But, borrowers might feel reluctant to liquidate collaterals since there are no incentive to do so.

- Liquidators exist to liquidate collaterals while getting incentives from a portion of the liquidated collaterals.