$LUNA & $UST 99% Crash: Keypoints of What Happened

What You Probably Want to Know on May 8th to May 12th, 2022 — A quick summary.

What You Probably Want to Know on May 8th to May 12th, 2022 — A quick summary:

- Mass liquidations of leveraged $UST and its depegging to below $1. Arbitrageurs flocked to swap their $UST for $LUNA in order to cash out — and this happened so fast that the circulating supply of $LUNA increased by more than 20x!

- On May 8th, the circulating supply of $LUNA was 346 million, and by May 12th, this number has increased to 7.1 trillion as users swapped $UST for $LUNA, increasing $LUNA’s selling pressure. $LUNA’s price has now been decimated to sub-zero from above $60 per token four days prior

- Terra network fell into extreme danger of being subject to 51% attack given that $LUNA price has fell by more than 90% (note that total $LUNA staked to protect the network is 240 million — at current market cap it will cost much less to attack the network). As such, Terra validators had halted the network fearing a potential governance attack following the aggressive inflation of its network token

- Centralized exchanges such as Binance and few others have decided to delist and cease trading of $LUNA and $UST pairs, although in May 13th, Binance announced introducing re-trading of $LUNA in which further minting will be halted

- MIM-UST pool in Curve protocol has been drained of $MIM, with 0.33% of $MIM left as of May 13th

We have compiled the keypoints of what you need to know to understand how this crash happened.

Firstly, what is $LUNA?

- $LUNA is the native currency of the Terra protocol

- Terra protocol is non-EVM blockchain that runs on Proof of Stake (“POS”) consensus mechanism. Validators need to stake $LUNA to earn block rewards from generating new Terra blocks. Before the 51% attack, Terra has a total of 130 validators and 240 million of $LUNA staked to protect the network

- As such, $LUNA also represents Terra protocol’s mining power, just like how Bitcoin miner hash power represents the pro-rata odds of generating new Bitcoin blocks in the Bitcoin network

- $LUNA is used to defend Terra stablecoin $UST’s peg to USD

- Holders were able to earn ~12% yield on $LUNA by delegating their $LUNA to validators for the purpose of validating Terra transactions. Previously this was doable on the users’ Terra Station wallet. $LUNA that are earning yield are called bonded $LUNA, denoted by $bLUNA. $bLUNA can be redeemed to $LUNA on 1:1 ratio basis after incurring a few days unbonding period

What is $UST?

- $UST is the native decentralized stablecoin of the Terra network that is designed to be algorithmic — meaning, its peg relative to USD fiat is maintained by utilizing another coin, in this case is $LUNA. The monetary policy of the Terra network is coded into a smart contract in which $LUNA is simply used to defend the $UST peg

- In ideal market condition, $1 of $UST should always equal to $1 USD fiat

- The value of $UST is driven by normal demand / supply relationship. When the demand of $UST is high, the protocol needs to issue more $UST and we refer to this event as expansion of $UST. When the demand is low and people are selling, the event is called contraction of $UST

How do $LUNA and $UST relationship work?

- Essentially, $LUNA is the counterparty for everyone who holds $UST. The system will accept $1 UST for $1 of LUNA irrespective of macroeconomic cycles in a 1:1 ratio i.e. to buy $1 worth of $UST, the protocol will mint $1 worth of $LUNA. Users can do this easily through the Terra Station wallet

- The system uses $LUNA to absorb the fluctuations of $UST. This means, whenever $UST’s value drops below the peg of $1, the protocol will algorithmically buy $UST (thereby taking them off the market permanently) and burn them until the peg is restored . The means to do this comes from minting / issuing new $LUNA and selling that $LUNA in the market. Conversely when the opposite is true i.e. $UST is worth above its peg, the protocol will algorithmically mint new $UST by burning $LUNA

- While the above peg defense mechanism is algorithmic, note that there needs to be participation of buyers and sellers in order to properly maintain the peg. People are incentivized to do as per algorithmically designed because of the arbitrage opportunity it presents. This means, if for example $UST falls below $1, say $0.90, then anyone can essentially obtain $1 worth of $LUNA for the price of just $0.90. The converse is also true if $UST is trading above its peg. Either way, there is always arbitrage opportunity

- The algorithmic model defend its own peg in the market without relying on overcollateralization of assets, like $DAI. It also naturally follows due to these features i.e. no depositors & backed by a single token, that $UST is not naturally redeemable for fiat the way other traditional types of stablecoins are. To zap in and out of $UST, you simply buy and sell $UST in the marketplace against another stable that is redeemable for USD, or swap to $LUNA to cash out

Implications of the $UST and $LUNA relationship:

- While it is not accurate to say that $UST is backed by $LUNA, it is important to understand that $LUNA needs to be minted to burn $UST whenever its peg falls. It means, if the peg falls fast, then there will be strong selling pressure on $LUNA ‘s price due to the new influx of supply. While in theory, the price and as such the market cap of $LUNA should not matter in relation to protecting the peg, as $1 of $UST will always give you $1 worth of $LUNA, it cannot be denied that the price and market cap of $LUNA is a reflection of people’s confidence in the system (recall that $LUNA is the native currency of the Terra network)

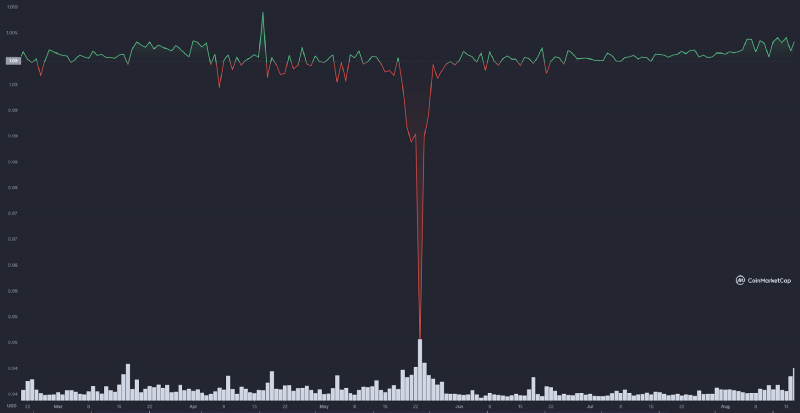

- We had a first taste of what can happen to $UST when its peg falls too fast and $LUNA’s market cap fell below $UST’s market cap as its price decline too fast. This happened before in 23 May 2021, as we can see from chart below. The issue was quickly solved by Terraform Labs purchasing $LUNA, thereby increasing its market cap again. This restored people’s confidence that purchasing discounted $UST to swap into $LUNA at 1:1 ratio

- Another implication is that during contraction events the protocol will mint more $LUNA to burn more $UST. In this case, Terra validators will be disadvantaged because their staked $LUNA holdings will be diluted as there are more $LUNA being issued in the system which will impact its price negatively. To solve for this problem, the protocol also algorithmically burn $LUNA as well during expansionary events. The implication is that the contraction and expansionary events would need to balance out to ensure that miners remain incentivized in the long-run i.e. it’s not ideal to be minting too much $LUNA over long period of time with no burning

What is Anchor Protocol and what is its significance?

- Anchor is a decentralized app (d’app) launched on the Terra network. It is a simple lending and borrowing platform in which users can deposit overcollateralized bonded assets e.g $bLUNA/ $bETH in order to secure $UST-denominated loan. Users with surplus fund could also deposit $UST into the d’app for a yield. It simply works like a bank, with difference in how the protocol charges borrowing interest

- Anchor Protocol is the largest protocol in Terra network. At its peak, Total Value Locked (“TVL”) in Anchor was north of US$30 billion, which represented ~15% of the entire DeFi TVL of ~US$200 billion. This gives you an idea of how the collapse of $UST and $LUNA impacted the entire crypto space, a market that has total market capitalization of US$2 trillion before the crash

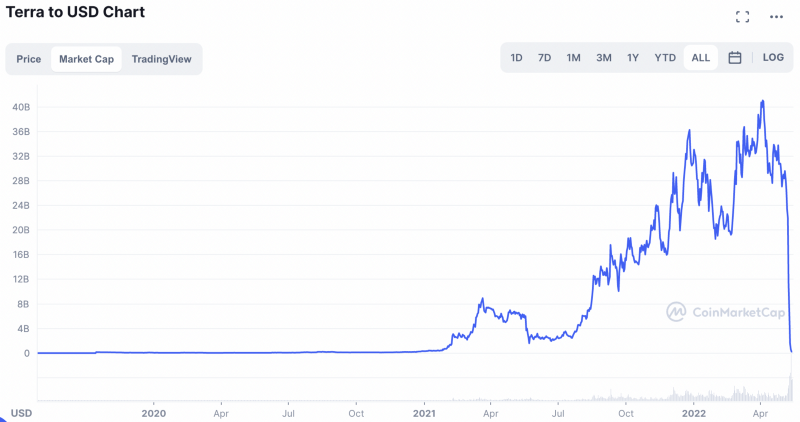

- Anchor Protocol, which historically offers 19.5%-20% yield on $UST, is the main demand driver of $UST, which drove its expansionary event from mid 2021 to April 2022. The expansionary $UST event means a lot of $LUNA has been burned, thereby increasing its value and market cap together with the increase in $UST’s market cap. As seen from charts below, at its peak there were US$18 billion worth of $UST in the system from just US$2 billion a year before, and US$40 billion worth of $LUNA from under US$10 billion a year before

What kind of problem is contributed by the Anchor protocol?

- Internally there are problems with Anchor as follows:

1) Not enough real demand i.e. not enough borrowers to compensate lenders. Terraform’s push to increase adoption of the Terra network using Anchor’s unsustainable USD yields has a huge role in starting the $UST expansionary event to $18 billion market cap in start of May 2022, as everyone wanted a piece of the 20% p.a interest on their USD Terra stablecoin

2) Over-leverage in the system that is already unsustainable suck reserves out of the system quicker than expected

Explanation:

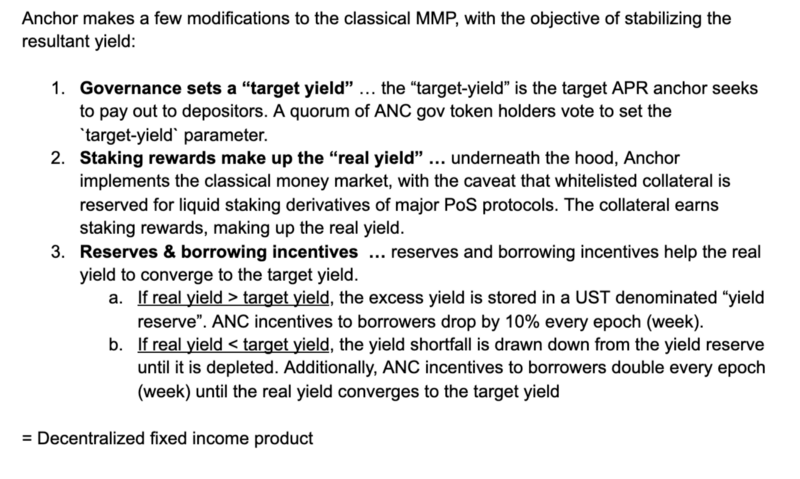

- Anchor protocol is ruled by its governance token, $ANC. It governs how much fixed interest will it be paying its depositors. The governance states that it will be paying depositors 19.5–20% of fixed interest — while in actuality it did not have sufficient borrowed assets to be paying the depositors such yield. The discrepancy is subsidized by the protocol reserves which was topped up by Terraform Labs (Do Kwon)

- Note that Anchor’s business model is a simple lending and borrowing platform — however it is not exactly the same as a bank as they don’t charge interest in a way a bank charges interest to its borrowers. Anchor takes bonded crypto assets and disbursed stablecoins loan to the borrower. As previously mentioned, bonded assets refer to yield-bearing assets. For example, $bLUNA refers to $LUNA that are being staked to earn yield — same with $bETH (bonded Ethereum)

- As such, Anchor does not explicitly charge interest to the borrowers. Instead, it takes temporary ownership of these yield bearing assets and pass on the yield from these assets to the lenders on the protocol

- Also note that Anchor takes overcollateralized bonded assets in return of stablecoins loan. Anchor sets the LTV to ~50%, which means a 12% yielding $LUNA were able to cover 24% p.a of $UST yield. That, of course, considering the total collateralized bonded assets are sufficient enough to cover the fixed lending rate. Three months before the crash, the protocol has US$ 5.5 billion of deposit and US$ 1.8 billion of borrowed value — hence it is very imbalanced. The difference is owing interest to the lenders are being taken from the Anchor protocol reserves, which was topped up by US$ 450 million in Feb 2022 (https://cointelegraph.com/news/terra-injects-450m-ust-into-anchor-reserve-days-before-protocol-depletion). Note that at the time of writing, total deposit is $UST equivalent of 2 billion while total borrowed is just $UST equivalent of 200,000. Yield reserves, meanwhile, has dwindled to a 30 days average of under $UST equivalent of 170 million

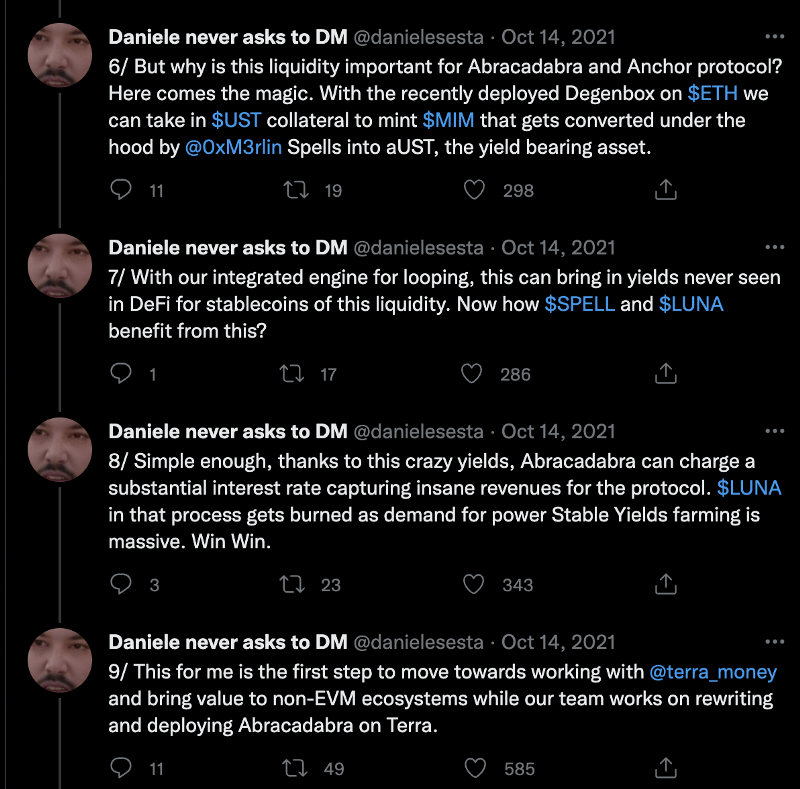

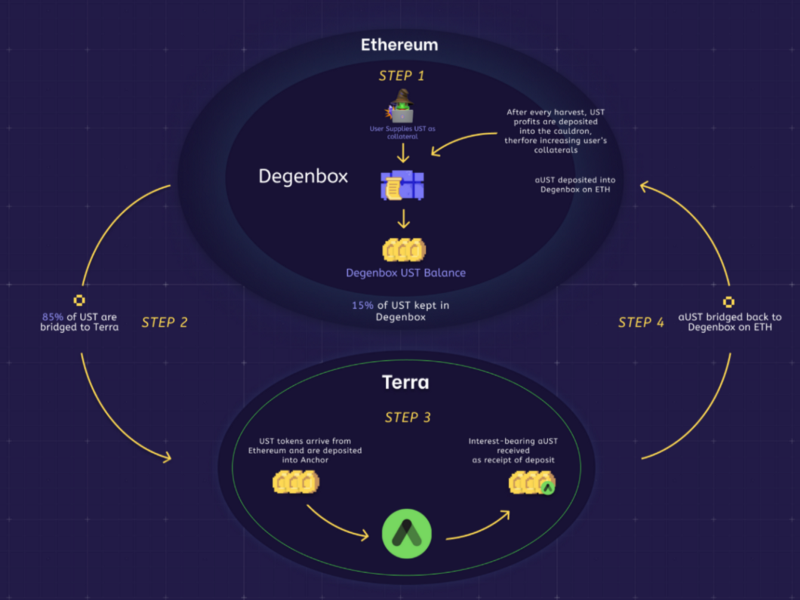

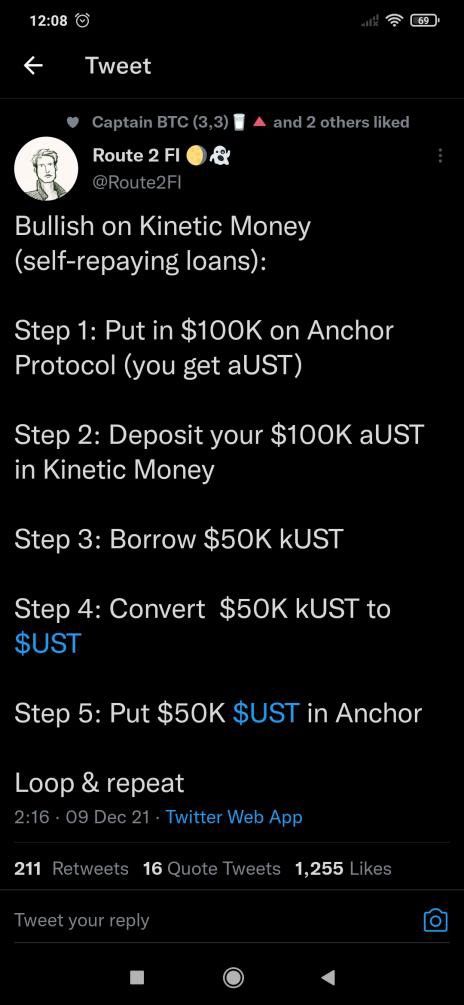

- In terms of overleverage, note that $UST is fully interoperable with other blockchains as well, in particular Ethereum. $UST is accepted as stablecoin collateral in Ethereum-based protocol, Abracadabra.money, to take out $MIM denominated loans (TVL of up to 90%). The borrower end up with $MIM, which they can use for their purpose which often includes converting back to $UST to withdraw more $MIM and hence more $UST, while Abracadabra, behind the scenes, take the collateralized $UST back to Anchor protocol to provide as lender, netting them $aUST (interest-bearing $UST). Abracadabra then deposits the profit into the ‘cauldron’, which increases the borrowers’ collateral which means they will be able to withdraw more $MIM with $UST operating in the backend. At that time the leverage seems “conservative” due to its lower probability of getting liquidated given the collateral is a stablecoin, hence its value seemingly will always be pegged. Abracadabra is not the only protocol too, with influencers such as Route2Fi promoting $UST collateralized leverage using in protocols such as Kinetic Money as well (it is also marketed as ‘self-repaying loan’!)

What are the implications on the problems of Anchor protocol?

- The implication is that for $UST to remain sustainable, someone (usually Terraform Labs) needs to keep topping up the reserves to subsidize the yield payable to lenders that are not currently fully covered by the yields on the collateralized asset

- If the reserves are not topped up, lenders will not be getting paid and the whole system may collapse with people getting out of $UST, putting pressure on its peg, which is made even worse by the super high level of leverage in the system. This will make sure the decline rate is fast — maybe even faster than the system can handle

- We know what will happen when there is selling pressure on $UST. If $UST started to trade below its peg, the system would need to defend the peg by burning $UST, achieved by minting $LUNA

- There is a limit on how much $LUNA can be minted in a day, hence there is a real risk of death spiral of $UST declined too fast and not enough people take opportunity to arbitrage $UST by buying it up

The system design flaw of LUNA and UST

- The main problem is that there is a limit on how much $LUNA can be minted in a day to prevent a death spiral as explained above. As such $UST redemption cannot happen at a rate that is faster than the rate $LUNA can be minted

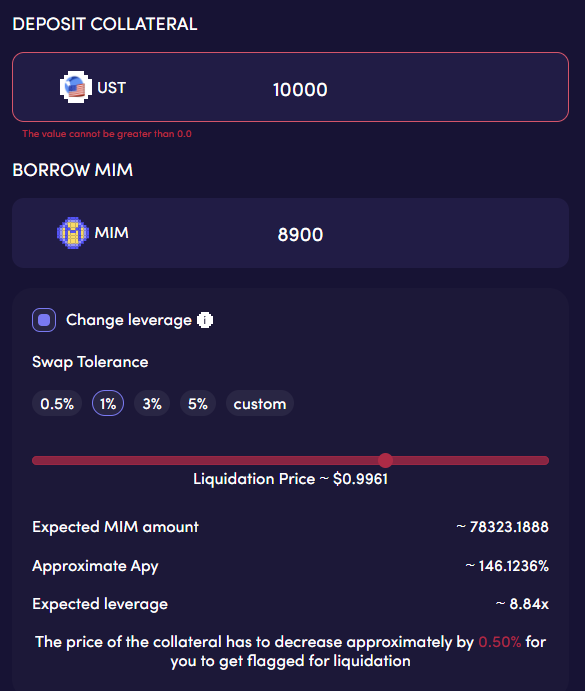

- The other problem is contributed by Anchor protocol, Abracadabra, and other lending protocols that accept $UST and $aUST as collateral, as they make the situation worse by helping issuing more $UST than what can actually be handled by the system. When $UST sufficiently depegged, mass liquidation in the system occurred. Note that a 0.5% move in $UST value is enough to trigger mass liquidation (see screenshot from Abracadabra below)

What about the purchase of Bitcoin reserves by Luna Foundation Guard (“LFG”)?

- Firstly, what is LFG? LFG is a Singapore-based DAO that supports the Terra network. They are a distinct organization from Terraform Labs, the Company behind the creation of $UST and $LUNA. LFG is a non-profit organization and its’ mandate is to promote the adoption of the Terra network

- LFG purchased US$1.5 billion worth of Bitcoin — $1 billion OTC swap with crypto prime broker Genesis and also $500 million of bitcoin from crypto hedge fund Three Arrows Capital. Both purchases were denominated in $UST. The Bitcoin reserves were meant to be used as reserves to defend the $UST peg, the native stablecoin of the Terra network

- When the $UST started to depeg, LFG liquidated all 42,530 Bitcoins in the reserve for $UST. It is a measure taken to protect the peg of $UST — which was opportunity for people to cash out their $UST, leaving the treasury wallet with no further bullets to protect the peg

- Overall the Bitcoin purchase for the treasury was a failed protection measure as LFG decided to liquidate the Bitcoin at a price lower than its acquisition

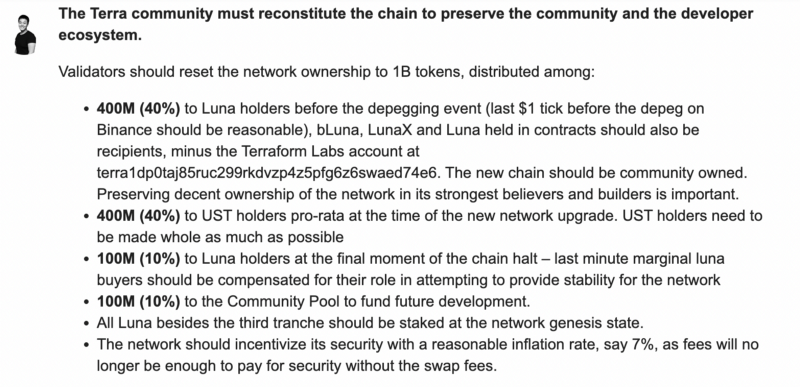

What’s being done to solve this? And what’s next?

- Terraform Labs have came up with the Terra Ecosystem revival plan (https://agora.terra.money/t/terra-ecosystem-revival-plan/8701)

- The plan involves creating a new chain in which the tokens will be reset to 1 billion from >7 trillion currently with the following distribution: