Should you invest in 1,500% APY?

Anything paying out 1,500% or some outrageous percentage APY is unlikely to be a sustainable project.

Summary:

- Anything paying out 1,500% or some outrageous percentage APY is unlikely to be a sustainable project. Also 1,500% APY is most likely to be largely denominated in native token, meaning as token holder, you are subject to a very large token inflation. Large token inflation means more tokens in circulation, and unless demand can keep up with the emission rate, it is likely to have negative impact on token prices

- Prices are very likely to get decimated when a project pays out that kind of inflation. Basic economic principles dictate that price is a function of supply and demand. When supply keeps piling up at a rate that is faster than demand growth, prices will be pressured downwards. Unless your share of tokens are growing as fast as its emission rate and prices do not fall faster than the emission rate, it is very difficult to make a profit in US$ terms

- All projects that manage its own treasury has to ensure that its treasury is growing at least at the same rate as its tokens’ emission rate, otherwise, benefits accruing to each token holder incrementally declines. The treasury book value also theoretically determines the lowest token price level — however token ownership does not necessarily entitle token holders to residual asset value of a project— so this price floor calculated from treasury book value often does not translate to reality especially during bear market / selloff event

Why is 1,500% APY a red flag?

- Understand that the principle of sustainability means that when a project pays you a yield, they must earn an ideally higher amount than what they are paying their stakers (you). This is important to ensure that the project is sustainable

- DeFi tokens are usually being priced in terms of another cryptocurrency token that is the native to the network it operates in (for example, $WETH in Ethereum network). Projects raised these tokens during the primary market offering or often called the Initial Dex Offering / Initial Liquidity Offering stage, while some being left in the liquidity pool to still provide for liquidity (earning transaction fees for the LP) in the secondary market. These tokens are then being managed by the DeFi project in order to earn sustainable return to pay DeFi token staker such as yourself!

- The problem is, there isn’t a lot of organic projects paying 1,500% APY. On average, liquidity pools are paying single digit APYs and while some borrowing / lending projects may be paying low single digit, it is still very far away from outrageous number like 1,500% APY. Unless the project aggressively uses leverage to boost its returns, 1,500% APY on sustainable basis is almost impossible (and if they do use leverage, this is something to be very cautious about)

- Also, when projects pay you 1,500% APY, it is very likely that these returns are being paid out in terms of the project’s native token. This means, the native token supply is growing at 1,500% APY while as mentioned above, the probability is low for the project to generate revenue growing at the same rate as its inflation. What this means is that incrementally, the benefits accruing to token holders are becoming less and less while the emission rate is likely to generate downwards pressure on DeFi token prices

- The only way for prices to keep pumping while inflation rate is very high to ensure that demand remains high i.e. there are a lot other people still pumped to buy into the project. However when demand slows down while supply keeps increasing at the same pace, prices will be affected

Go through the checklist before you invest:

- The 1,500% APY that the project is paying — what currency is this denominated in? Note that most degen projects will be paying 1,500% APY of their own native token as mentioned above. For example, Wonderland protocol pays you $TIME token, which cost the protocol next to nothing to mint. However, investors paid currencies such as $AVAX to purchase $TIME, which are then used by the protocol to generate the returns to maintain the treasury’s book value

- Where is the project generating return and how much is the level of return?

- You can easily check the project’s wallets in Etherscan (for projects in Ethereum network) and check this against d’apps such as www.zapper.fi to scan briefly where the project is generating its return

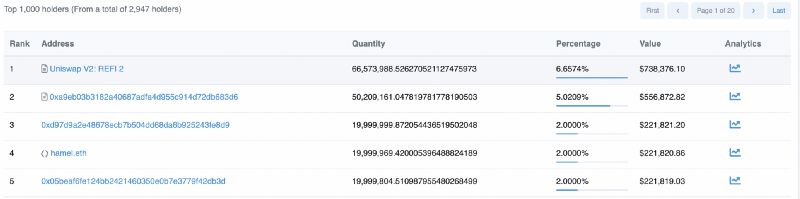

- Let’s take an example — below is the Etherscan screenshot of Reimagined Finance (ReFi)’s token holder page. From this page we understand that the $REFI token has 2,947 holders. Let’s look at the top 5 holders below:

- (cont’d):

- The first two holders are contract addresses as indicated by the icon before the name. The first holder is Uniswap trading pool. We understand this pool has US$1.47 million of liquidity consisting of almost 68 million $REFI and 391 $WETH. The second one is a wallet belonging to the project holding only $REFI

- (cont’d):

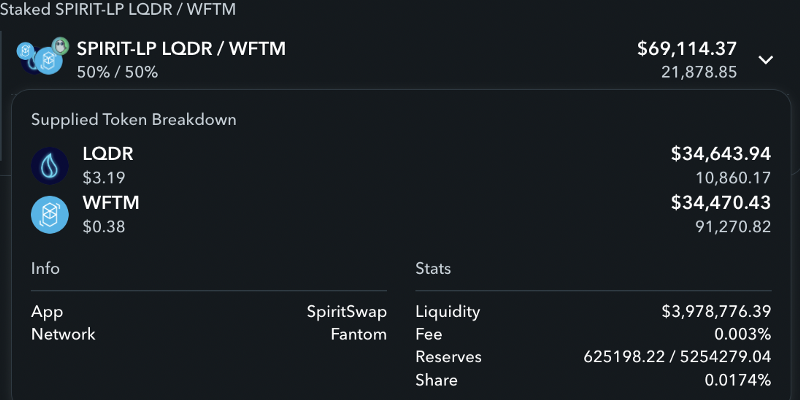

- The third address in the Etherscan screenshot is one of the protocol’s wallet. We can see from the screenshot below that this wallet has ~20 million of $REFI tokens worth $221,477. Meanwhile the wallet is generating yield in LiquidDriver in the Fantom network by providing liquidity in the $LQDR-$WFTM pool earning 0.003% fee for all transactions happening in the pool. The amount of liquidity provided to the pool is US$71,238

- How does the project calculates its APR or APY? After you are familiar with where and how the project is earning its returns, you need to check for how the project calculates its yield to identify any red flags, if any. Let’s take a look at few examples:

(1) Buying / lending protocol types with one yield-generating asset as denominator (e.g Aave)

APR = (Reward per seconds * no of seconds in a year* Reward price / wei decimals*) / (total token supply * token price / wei decimals*)

APY = (1+APR / no of seconds in a year)^no of seconds in a year -1

(2) Yield farming d’apps where LP provide equal liquidity in two assets:

Yield farming protocols in general will have the following parameters which is used to calculate the APR or APY. If we take Pancakeswap as example, the calculation is as follows:

APR = Fee share per year / total liquidity

Whereby

Fee share per year = 24 hour volume* fees* 365

Of course with other yield farms, the calculation may be different i.e. fee share may not be calculated by 24 hours volume, etc

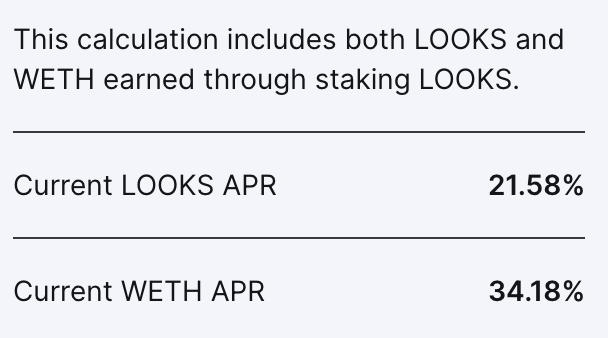

- Is the yield autocompounding? Note that the general rule of thumb is that if the yield is autocompounding, the rewards are being reinvested into the native token / token being invested for more of the tokens. As such, if the rewards token is what you are interested in harvesting, generally autocompounding will not be suitable for you. For example, NFT exchange Looksrare shares 100% of its $WETH revenues to all of its token holders. They also offer both staking and autocompounding options. If you take the staking options, your $LOOKS will be growing at 21.58% APR while your $WETH rewards will be growing at 34.18% APR. Meanwhile if you take the autocompounding options, you will need to forgo your $WETH rewards as the $WETH harvested will be automatically converted into more $LOOKS. In this case total $LOOKS APY calculation will be (1+ WETH APY)*(1+ LOOKS APR)-1

Summary of red flags:

- Revenue generation (either from treasury growth or revenues from lending etc) is much lower than token inflation & expenses. For example, Anchor protocol is very imbalanced when it comes to the amount it pays its lenders vs the amount it receives from its borrowers

- Rewards are only in form of native token with no other token rewards. For example, investing in Wonderland Finance only yields you $TIME (albeit at 18,000% APY)

- When analyzing where the treasury of the protocol is being invested in, you find there are substantial leverage involved

- APR or APY calculation is very much driven by token inflation rather than rewards